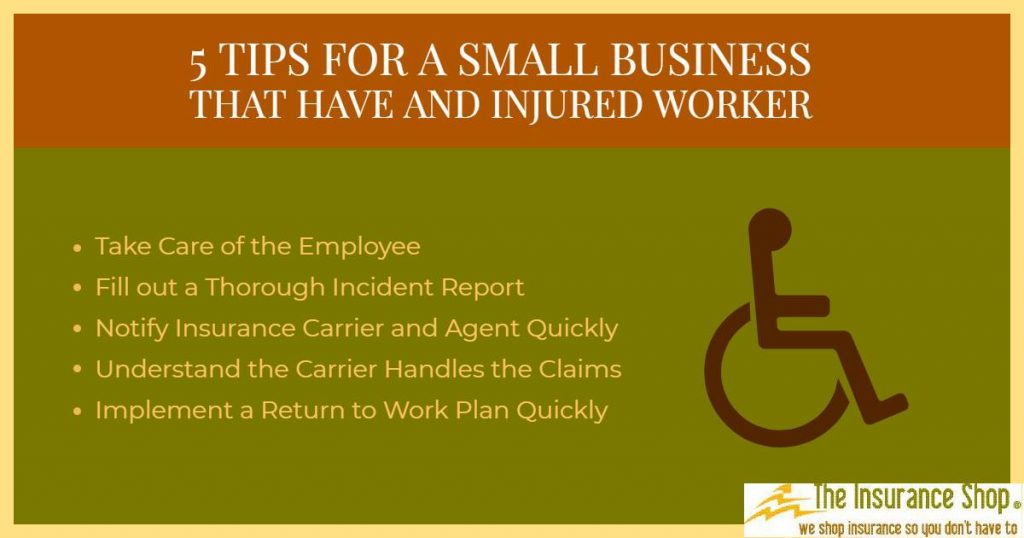

5 Types of insurance every Real Estate Agency should have.

Real Estate Agencies take on a unique set of risks compared to other traditional businesses. Many businesses, like a restaurant for example, have a brick and mortar location where a majority or all of the business takes place. Real Estate Agencies, while most do have a physical address, have a majority of their work taking place at a third party location. These locations frequently are at the property they are helping to sell. For this reason, real estates agencies have to secure a unique group of coverages in order to adequately protect their business. Here are 5 recommended coverages most real estate agencies should secure.

- General Liability Coverage

- Errors and Omissions (Professional Liability)

- Property Insurance

- Hired and Non-Owned Auto

- Workers’ Compensation Insurance

General Liability Insurance

For most real estate agencies, the risks related to general liability coverage are often minimal. This is primarily due to not much business occurring at the physical location. A majority of their work is done over the phone, by electronic mail or at a third party location. Off-Premises risks can be extensive for this industry. That is true whether you are dealing with the selling of properties or rental properties. These risks typically arise from sales visits, inspections, open-houses and similar work done at the customers’ home or other buildings. In some cases, there is an agent representing both the buyer and the seller. Any damage that occurs during joint operations, like an open-house, can cause a dispute between all parties involved. Monitoring of keys is another risk that must be dealt with carefully. Documenting every time, you access a facility is highly recommended to limit the risk you face regarding access to the facility.

Errors and Omissions Coverage (Professional Liability)

Exposure associated with errors and omissions (E&O) may be the most significant risk a real estate agency faces. This is because a majority of the work you do is highly specialized and you are giving advice. If you give the wrong advice, it can cause the business to be liable to the client in the future. To limit these risks the agency can make sure all employees have the proper credentials, experience and has the proper ratio of professional employees to clerical employees. Thorough background checks are essential to limit E&O Claims.

Commercial Property Insurance

If your agency owns physical property, you need to secure Commercial Property Insurance. There are two ways these policies are sold. They are sold on a replacement base or on an agreed upon value of the property. In most cases, it is better to secure a policy at replacement level. This will include the cost to tear down the facility, remove all debris and build a new facility. If your policy is an agreed upon value it typically does not include these additional costs.

Commercial Auto/Hired and Non-Owned Auto Coverage

If you own vehicles for your employees to use when they are away from the office than you need to secure a Commercial Auto Policy. Most real estate agencies do not own vehicles specifically for company use, but they do have agents who use their personal cars for business purposes. When these employees are using their personal vehicles for business purposes the business is liable for any accidents that may occur. The business is not liable for the damage to the employee’s car. This is covered by the employee’s personal auto insurance policy. The business is liable for damage to the car and any bodily injuries that may occur to third parties. A Hired and Non-Owned Auto Insurance Policy will take care of most liability a business faces resulting from accidents that occur when employees drive their personal cars or rented vehicles for business purposes.

Workers’ Compensation Coverage

Workers’ Compensation Insurance is required by law in 48 out of 50 states. Each state has their own rules and regulations regarding the administration of this system. Each state has their own exceptions for some small or family owned businesses. Workers Comp is similar to general liability, except that it covers employees and not third parties. When an employee is hurt on the job, work comp coverage will cover some of their lost wages (typically 60%) and medical costs incurred as a result of the injury.